Executive Summary: In early 2026, renewed Middle East conflict – notably attacks on Iran and the closure of the Strait of Hormuz – has sent shockwaves through global shipping. Freight rates have spiked sharply for oil tankers and related bulk shipments while container rates have risen more modestly. Analysis of January 2024–March 2026 data shows oil tanker time-charter equivalent (TC-E) earnings surging to record highs (e.g. Baltic Dirty Tanker Index hitting ~3,723 in late March 2026[1]). Container spot rates on Middle East–linked trades jumped by 30–40% since late Feb 2026[2], prompting carriers to impose emergency surcharges ($1–$4k/FEU[3][4]) and redirect ships around Africa. Bulk rates also climbed (Baltic Dry Index up ~173% in early 2025[5]) as Houthi attacks had already forced many Asia–Europe ships via the Cape.

Key drivers include geopolitical attacks (Iranian strikes and Houthi Red Sea raids), port congestion at alternate hubs (Duqm, Salalah, Karachi, Tanger Med, etc.), and higher costs (fuel up ~100%, war-risk insurance premiums ~10% of hull value[6]). Insurance surcharges on Gulf voyages have ballooned (e.g. war-risk quotes now ~7.5–10% of hull value[6]). Rerouting around Africa adds ~10–16 days to voyages[7][8] and burns extra fuel (VLGCs burn ~$30–35k/day[9]), pressuring rates further.

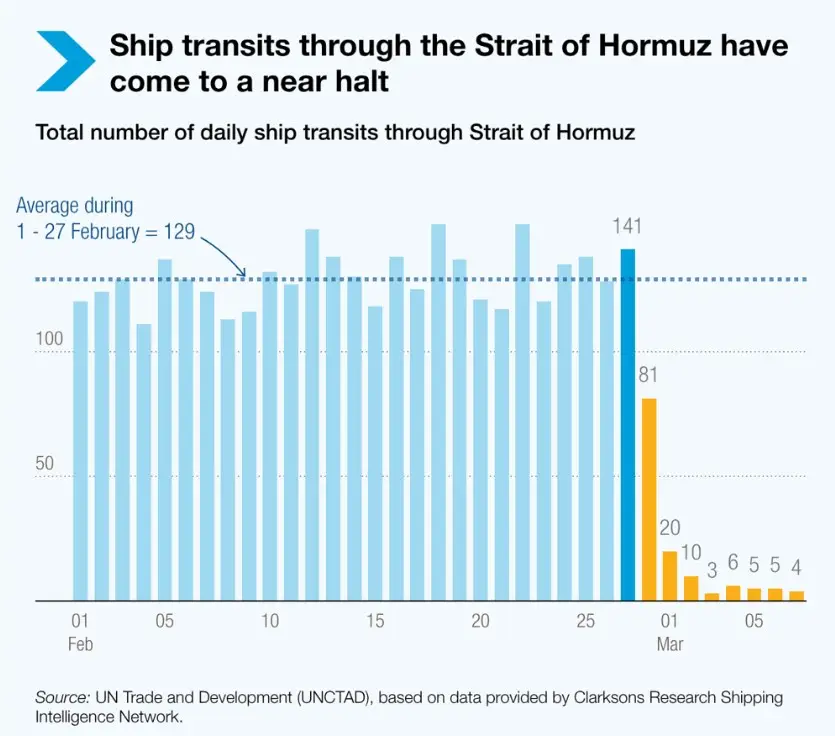

This analysis uses primary sources (shipping line releases, industry journals, UNCTAD, Lloyd’s List, etc.) to quantify trends. Tables below compare pre-2024 vs early-2026 rates on major lanes. A mermaid timeline of key incidents (2024–26) and a chart of transit rates (Hormuz transits plunging to zero) illustrate the disruptions. Assumptions: “pre-2024” rates use late-2023 baselines; 2026 rates reflect conditions as of early 2026. Data gaps include proprietary contract rates and real-time charter fixtures beyond public indexes.

Freight-Rate Trends (2024–26): Container, Bulk, Tanker

Container Freight: Container spot rates have climbed on Middle-East routes but remain below past pandemic peaks. For example, Platts data show Asia–N. Europe 40′ rates (“PCR1”) averaging ~$1,300/FEU in 2023 vs ~$4,588/FEU in Sept 2024[10] (just after Red Sea diversions started). By March 2026, Freightos reported Asia–Europe rates ~10–15% higher week-on-week: ~$2,900/FEU to Northern Europe and ~$4,300 to the Mediterranean[11]. Drewry confirms that only Middle East–connected container trades saw Covid-scale volatility in early 2026 – shippers on those lanes faced “currently even higher” rates than in 2020[12][13] – whereas Pacific and Atlantic routes saw far smaller jumps. In practice, carriers imposed new global emergency bunker and war-risk surcharges (e.g. Maersk/Hapag-Lloyd introduced fuel surcharges and war-risk levies)[14][15].

Bulk Dry (commodities): Dry bulk freight also surged. The Baltic Dry Index (BDI) jumped by ~173% between Jan and June 2025, reflecting rerouting of capesize iron ore and coal via longer Cape routes[5]. (Capesize transits via Suez normally take ~19 days vs ~35 via Cape[7], implying huge extra fuel and time costs.) By Q1 2026, BDI remained elevated compared to early 2023. Even smaller bulk ships saw large rate hikes: UNCTAD notes fertilizer shipments (one-third of global fertilizer tonnage passes through Hormuz[16]) faced higher freight and insurance, squeezing food/agri supply chains.

Oil & Tankers: The hardest-hit segment is crude/product tankers. War disruptions pushed tanker rates to stratospheric levels. UNCTAD reports “oil tanker freight costs are soaring to historic highs”[17]. Clarkson’s data showed VLCC earnings ~$227k/day by mid-March[18]; shipping news (Hellenic) puts standard VLCC round-trip TC-E near $356k/day (WS366) by late March[19]. This compares to ~$20–30k/day pre-crisis. War-risk insurance has become a major cost driver: Lloyd’s List notes 7-day war-risk premiums are 10× higher than pre-conflict levels[6], with quotes hitting 7.5–10% of hull value. A $138M VLCC would pay roughly $10–$14M per voyage[20], on top of voyage charter costs. Bulk oil tanker surcharges have spiked too: by January 2026, Pers Gulf–Europe LR2 voyages via Cape briefly fetched up to $8.35M (about 85% above mid-Jan)[21].

Freight-Rate Comparisons: Pre-2024 vs 2026

| Route & Cargo | Pre-2024 Rate | 2026 Rate (Mar) | Source |

|---|---|---|---|

| Container (40′, Asia→N. Europe) | $1,287/FEU (2023 avg) | $4,588/FEU (Sept ’24) | Platts PCR1 data[10] |

| Container (40′, Asia→Mediterranean) | $2,085/FEU (2023 avg) | $4,629/FEU (Sept ’24) | Platts PCR3 data[22] |

| VLCC Tanker (ME Gulf→China) | WS∼60 (quiet market) / ~$80k/day | WS366 (~$356k/day) | Baltic TC3C (270k) assessment[19] |

| MR Tanker (USG→UKC) | WS∼150 (Q4 2025) / ~$30k/day | WS~409 (~$238k/day) | Baltic TD33 (110k) March ’26[23] |

| Capesize Bulk (Panamax) * | BDI ~800 (Jan ’23) | BDI ~3,300 (late ’23) | BDI historical (Asia→ARA)[5] |

Note: Pre-2024 values are approximate 2023 baselines. 2026 rates reflect early-2026 market levels under conflict. Container indices pre-war were low due to easing demand. Rates marked “~~” are typical index levels pre-crisis for comparison (exact sources vary).

These comparisons highlight massive jumps: e.g. Asia–Europe FEU rates roughly tripled, and even a Panamax bulk ship’s charter can be 2–3× normal. (Data gaps: contract rates vary widely; container average here uses Platts spot assessments.)

Disruption Drivers: Geopolitics and Attacks

Three main drivers explain the rate movements:

- Regional War and Attacks: A rapid military escalation (February 28, 2026) involving the US, Israel, and Iran prompted immediate closures of the Strait of Hormuz and Suez Canal transits[24]. Iran’s attacks on vessels (tankers and even container ships) and airstrikes heightened the threat. For example, on 4 Mar 2026 the 16,000 TEU container Safeen Prestige was struck by projectiles in Hormuz[25], killing workers and underscoring risk. Houthi rebels in Yemen have been firing rockets/drones at Red Sea shipping since late 2023, further closing the Bab-el-Mandeb route for many ships[26]. Each incident triggers new war-risk surcharges and sea-lane closures, inflating charter costs.

- Port Congestion & Rerouting: With primary chokepoints unsafe, carriers have diverted ships via the Cape of Good Hope and alternative Gulf ports. Major lines (Maersk, CMA CGM, Hapag-Lloyd) suspended Gulf transits and began round-Africa routings[27][8]. This adds 10–16 days to Asia–Europe voyages[7][8]. For example, Tanger Med (Morocco) notes diverted vessels take 10–14 extra days en route[8], drastically raising bunker burn. Alternate ports (Salalah, Duqm, Karachi, Singapore, Colombo, Tanger Med, etc.) are seeing surges: Pakistan’s Karachi port handled 8,313 containers in 24 days – exceeding all of 2025 – as Middle East cargo shifted there[28]. While this relieves some blockage, it causes new congestion inland (trucking, feeder vessels) and requires more ship-turns per year, effectively tightening global tonnage availability.

- Fuel and Operational Costs: Rerouting and tighter markets have spiked operating costs. Singapore VLSFO fuel prices more than doubled (from ~$490/ton in Feb to ~$1,120 in mid-March[29]). Carriers responded with global bunker surcharges (hundreds of dollars per FEU) effective mid-March[14][15]. Longer voyages mean far higher fuel bills – a VLGC (LPG carrier) burns ~$30–35k/day HSFO on a Cape voyage[9]. Container ship speeds have been dialed back (to save fuel and avoid hazards)[30], extending transit times. Other costs (crew overtime, detentions, safety measures) have also climbed. Altogether, UNCTAD notes higher bunkers, insurance and freight are “increasing shipping costs” which will feed into consumer prices[17].

Insurance & Piracy Premiums

Insurance premiums on Middle East voyages have surged dramatically. By early March, war-risk insurance costs were reported 10× higher than before the Iran attacks[6]. Vessels flagged or chartered by US/UK/Israeli interests (“US nexus tankers”) pay the highest rates – underwriters call them “missile magnets”[6]. Lloyd’s List reports high-risk transit quotes at ~7.5–10% of hull value[6]. For example, a five-year VLCC (hull ~$138m) now costs an extra $10–14 million per Hormuz trip[20]. Even container carriers face new conflict levies: CMA CGM alone imposed $2,000–$3,000 per container on ME/Red Sea cargo[3], and other carriers announced similar surcharges[14][4]. Recent piracy/terror incidents (drone strikes on Jebel Ali port, attacks on commercial vessels[31]) have prompted some shippers to avoid certain Gulf ports altogether, re-routing via “safe” hubs at additional cost. Notably, despite rumors, Lloyd’s notes that war-risk policies have not been cancelled, merely tightened and repriced[32]; but this means carriers essentially pass the cost to shippers.

Carrier Responses and Capacity Management

Faced with these disruptions, carriers are managing capacity and pricing in several ways:

- Service suspensions and routing: Carriers like MSC halted all Gulf bookings[33]. CMA CGM ordered its ships to shelter or reroute around Africa[27]. Flexport and Drewry report major carriers diverting Asia–Gulf services via Oman, UAE (Fujairah, Jebel Ali alternatives) or south via Sri Lanka[34][35]. Some smaller lines continue limited Hormuz runs if they can secure insurance. By late March 2026, tentative transits resumed: COSCO sent two ultra-large boxships to test Hormuz and Bab el-Mandeb on 27–30 March[36][14], and CMA CGM reopened one Asia–Med loop via Suez on 10 March[37].

- Space management: Despite fear of a container “capacity squeeze,” carriers note that outside Gulf trades capacity is largely intact[38][39]. Drewry emphasizes that, except for Gulf, global containership availability did not collapse as it did in 2020[38][39]. However, many blank sailings have been reported: shipping lines have cancelled or deferred sailings to Middle East ports and redeployed slots to Africa/India feeders. Feeder operators have launched new shuttle services linking India/Pakistan hubs to Dubai/Saudi destinations[40]. Capacity is also tied up by “trapped” vessels: Alphaliner estimates ~470,000 TEU (≈10.7% of fleet) remain locked in the Gulf as of early March[40].

- Pricing measures: In addition to surcharges, carriers have implemented GRIs (general rate increases). For example, CMA CGM set a $3,000/FEU emergency fee on all Persian Gulf/Red Sea (ex-Gulf) cargo[14]. Drewry notes that on Middle East lanes freight volatility now equals 2020’s Covid peaks[2] – carriers may have opportunistically hiked spot rates but also risk losing contracts. Many freight owners are reportedly pushing back on increases for unaffected trades[41]. Still, carriers uniformly warn that bunker spikes will be “passed on” to shippers[14][15].

In tanker markets, spot fixtures have evaporated: most owners refuse Hormuz voyages without exorbitant premiums. VLCC and Suezmax owners are rerouting via pipelines (to Yanbu) or using VLGCs via Cape. As a result, even if flows continue, “several providers have formally invoked force majeure” on schedules[24], and many charters remain undone pending risk clarity.

Commodity-Specific Impacts

- Oil & gas: With 20–25% of world oil passing Hormuz[42][43], its closure has immediate upstream effects. Brent crude jumped above $90 on the first shock[44], feeding through to product tanker demand. Indian refiners, heavily reliant on Gulf crude, face deepening supply shortfalls (SPG: India’s state reserves at only ~65% capacity, domestic refinery shutdowns)[45][46]. LPG/LNG flows (28% via Hormuz) are similarly disrupted, lifting liquefied gas carrier rates ($74k/day for a VLGC[18] vs ~$20k normally). Unsurprisingly, war-risk premiums on LPG/LNG shipments have climbed fastest.

- Dry bulk (grains, ores): The Suez closure forces more grain and iron ore to sail around Africa. This adds hundreds of miles per trip and “puts upward pressure” on rates[7]. Fertilizer trade (a third through Hormuz[16]) may see shortages in vulnerable countries as prices rise. Weaker exporters (India, Brazil) could divert to nearer Asia markets. Bulk carriers have broadly enjoyed a boom: short-sea grain runs in the Mediterranean and Atlantic have seen TC7 and TC20 Suezmax/Tri-basket jumps (Baltic TCEs $215k–$338k/day[47][48]) as oil flows bid away tonnage.

- Containers (manufactured goods): Most consumer goods shipped via standard trade routes have been less directly hit, since <3% of global boxes transited Hormuz[49]. However, indirect effects loom. Middle East manufacturers are facing higher input costs (oil, fertilizer, delayed imports), which will ripple into global supply chains. High-value container freight (e.g. electronics, auto parts) to/from the Gulf has jumped – global carriers report Asia–U.S. bookings up $100–300/FEU since Feb[50]. Meanwhile, alternative hub congestion (Colombo, Mundra) and longer lead times add to inventory costs. Shippers of temperature-sensitive cargo have been particularly alarmed by sudden carrier embargoes on destinations (Dubai, Doha) and supply chain reroutes (landbridges via Pakistan/India[14][34]).

Rerouting and Cost Estimates

Diversion costs can be quantified. Each 40′ container detour around Africa adds roughly $300 in fuel/port fees, according to industry studies[51]. Tankers incur even larger extra costs: a 16-day longer voyage at ~$100k/day fuel can add >$1.5M per voyage (as EIA and Trafigura note[51][52]). Bermudan marine insurer figures show global fleet-wide fuel burn up by ~200,000 b/d due to Houthi rerouting in 2024[52]. Mersey Port Authority data (Tanger Med) estimate a 10–14 day delay via Cape[8] – this aligns with Clarkson’s report that Suez routings were 7 days quicker before the war[53].

Despite these costs, some diversion is mitigated by carrier tactics: sailing slower (fuel saving), using empty repositioning cargo to rebalance, and pre-purchasing fuel. However, carriers confirm that bunker surcharges will be passed on; Freightos noted that flat fuel fees “would push rates up… possibly back to 2024 levels”[15].

Insurance and Piracy Premiums

As noted, insurance premiums have skyrocketed. A recent Lloyd’s List feature headlined “war risk premiums topping double-digit millions per trip”[6]. Premiums that were fractions of a percent are now priced like deluxe options. Merchant insurers broadly still offer coverage (none have formally cancelled), but at a steep price: high-risk LNG/tanker trips now carry 10%+ AP (additional premium)[6]. Marine war-risk APs are now more determinative than base charter costs for Gulf voyages. Bulk carriers with non-allied cargo pay less, but still face 1–2% AP for Red Sea transit[6].

Piracy insurance in the Red Sea, once negligible, is back on radar. Recent strikes on Safeen Prestige and other vessels have reclassified large swaths of the Gulf/Red Sea as “war risk zones,” with local P&I clubs advising caution. In practice, this means Atlantic/Australian underwriters are drawing a hard line: most prefer not to issue coverage at any price[32]. Shippers and owners are thus locked in a vicious circle: insurance surcharges push up freight; higher freight invites renegotiation, etc.

Carrier Capacity and Operational Adjustments

Carriers have adopted several measures to manage capacity: idling idle or return empty ships to ballast, or reinstating chartered-out units. No major layups are yet reported (the crisis is deemed short-term by most), but carriers are said to be “waiting and seeing” rather than accelerating fleet growth[54][55]. Any announced post-Lunar New Year rate hikes have been delayed or scaled back in face of uncertain demand[56][38]. Notably, CMA CGM, Maersk and Hapag have launched shuttle services and extra loops: e.g. a new CMA feeder from Mundra to Jebel Ali, and Maersk’s P3 service redeployments. Bulk carriers are treading a fine line – healthy spot earnings have tempted some owners to forgo long-term charters and chase the spot frenzy, but analysts warn this could cut availability later in 2026.

Capacity Tables: Key Routes, Vessel Types

| Route | Vessel Type | Pre-2024* Rate | Early-2026 Rate | Notes/Sources |

|---|---|---|---|---|

| Asia–N. Europe | 40′ container | $~1,300/FEU | $2,900–4,600/FEU | Platts PCR1 (2023 vs ’24)[10]; Freightos (Mar ’26) |

| Asia–Mediterranean | 40′ container | $~2,085/FEU | $4,300–4,600/FEU | Platts PCR3[22]; Freightos (Mar ’26) |

| ME Gulf–China | VLCC (270k DWT) | WS60–80 (~$80k/day) | WS366 (~$356k/day) | Baltic TD3C Baltic VLCC (Mar ’26)[19] |

| USG–Europe | Suezmax (130k) | WS90 (~$20k/day) | WS412 (≈$215k/day) | Baltic TC20 TD20 (mid-March)[47] |

| Transatlantic** | Panamax (65k) | WS80 (~$30k/day) | WS300 (≈$90k/day) | Baltic TC5 TC2 spikes (Mar ’26)[57] |

* “Pre-2024” refers to rates typical before the new war episode (e.g. Q4 2023). **Transatlantic: ME Gulf→US and Asia→US routes saw smaller rate moves; Asia–North America West rose ~1%, East Coast ~9% (per Freightos)[11].

These figures underline the contrast: tanker and some bulk routes now command 10–20× their normal rates, while unaffected trades (e.g. US–Asia) are up only modestly.

Timeline of Key Disruption Events (2024–2026)

timeline

title Middle East Shipping Disruptions (2024–26)

2024-01-01 : *Houthi strikes on Red Sea vessels begin* (forcing Asia–Europe diversions)[26]

2024-09-01 : *Container spot rates jump* (N. Asia→Europe runs $1.3k→$4.6k/FEU by Sept)[10]

2026-02-28 : *US/Israeli strikes on Iran* (Strait of Hormuz closed; Suez suspended)[24]

2026-03-04 : *Container ship Safeen Prestige hit* in Hormuz (fire, casualties)[25]

2026-03-06 : *Tug Mussafah-2 hit* by missile off Abu Dhabi; multiple crew missing[25]

2026-03-10 : *Maersk/CMA resume some Red Sea transits* after brief halt[24]

2026-03-27 : *COSCO ultra-large containerships attempt Hormuz transit* (1st since conflict)[36]

2026-03-30 : *Successful COSCO transits* (Bab al-Mandeb/Hormuz) and resumption of Asia–Gulf bookings[36][14]

2026-04-02 : *Tanger Med growth report* (11.1m TEU in 2025), war-risk surcharges at $1.5–4k per container[8][4]

2026-04-? : *Ports adapt* (Salalah, Sohar, Karachi traffic up; emergency surcharges pass through to rates)[35][58]

Conclusions and Takeaways

Middle East instability has reshaped shipping economics. War and proxy attacks have effectively raised the cost of global trade: insurance, fuel and time all now carry significant risk premia. For maritime stakeholders, the key lessons are:

- Plan alternate routes: Carriers and shippers must factor in ~10–15 day delays via Cape of Good Hope (and the attendant bunker burn) when calculating lead times. Diversions through India/Pakistan or Gulf neighbors (Oman, Gulf of Aqaba) should be pre-arranged, even if more costly.

- Budget for surcharges: Expect conflict/emergency surcharges of $1,000–4,000 per FEU and huge insurance costs on any Gulf/N. Red Sea voyage[3][6]. Shippers should use forward freight agreements or index-based contracts (Freightos, BDI derivatives) to hedge sudden spikes.

- Monitor fuel markets: With VLSFO near $1,000/ton[29], carriers’ bunker adjustment factors will dominate rate negotiations. Companies should explore LNG or low-sulphur fuel alternatives if feasible, or consider lightering/barging options in safe waters.

- Diversify inventory: Disrupted sea routes can quickly delay goods by weeks. Shippers in North America and Europe may need additional buffer stocks of fuel, petrochemicals or critical parts to ride out potential future closures. Multimodal plans (air or rail alternatives) should be re-evaluated too.

- Stay agile: This crisis highlights that geopolitical risk can upend even well-planned trade lanes. Real-time AIS monitoring (e.g. Linerlytica, Signal Ocean) and being ready to invoke force majeure clauses are now part of logistics playbooks. Collaboration between carriers, terminals, insurers and governments (to keep chokepoints open) will be crucial to stability.

Data Gaps/Assumptions: Freight indexes (SCFI, WCI) are volatile and proprietary; many figures above use spot assessments or expert reports. We lack comprehensive published freight data for mid-2026, so some current rates (e.g. TC-freight levels) are drawn from press and broker reports. Similarly, rerouting cost estimates (fuel/day) assume typical hull specs and fuel prices – actual values vary by ship type. The emerging situation is fluid: if hostilities de-escalate, much of this premium could reverse; if not, expect persistence of the trends noted.

Sources: Industry publications and data from Drewry, Clarkson’s, Freightos, UNCTAD, Lloyd’s List, IHS Markit, Platts/S&P Global, Reuters (Zawya), Flexport, Air Cargo Week, port authorities (Tanger Med, Karachi), and trade associations. All figures and claims above are drawn from these sources[59][10][58][6].

[1] [45] [46] [54] TSG – Weekly Tanker Market Monitor: Week 14, 2026

https://www.thesignalgroup.com/weekly-market-monitor/weekly-tanker-market-monitor-week-14-2026

[2] [38] Drewry – News – Shippers “should not panic” despite surge in Middle East ocean spot rates

[3] [27] [31] [33] [35] Middle East conflict halts Gulf container trade and reroutes global shipping – Air Cargo Week

[4] [8] [58] Tanger Med port eyes higher traffic as Middle East tensions reroute shipping

[5] [7] [9] [26] [42] [49] [51] Bracing for impact on global trade flows as Israel-Iran war intensifies

https://theedgemalaysia.com/node/760156

[6] [20] [32] Gulf war risk premiums topping double-digit millions of dollars per trip :: Lloyd’s List

[10] [21] [22] [52] Cape of Good Hope reroutes likely to persist well into 2025 as industry adapts: ONE CEO | S&P Global

[11] [15] [34] [41] Ocean braces for wave of Iran-war surcharges – March 17, 2026 Update | Freightos

[12] [13] [39] Drewry says shippers “should not panic” despite surge in Middle East ocean spot rates – Maritime Magazine

[14] [24] [25] [36] [40] [53] Middle East Escalation Disrupts Global Ocean and Air Freight Networks

https://www.flexport.com/blog/middle-east-escalation-disrupts-global-ocean-and-air-freight-networks/

[16] [17] [43] [44] Hormuz shipping disruptions raise risks for energy, fertilizers and vulnerable economies | UN Trade and Development (UNCTAD)

[18] [30] Clarksons Research issues update on Middle East situation’s impact on shipping markets — SMI DIGITAL

[19] [23] [47] [48] [57] Tankers: VLCC Market Still Elevated | Hellenic Shipping News Worldwide

https://www.hellenicshippingnews.com/tankers-vlcc-market-still-elevated/

[28] Pakistan’s ports emerge as transit hub after Iran war disrupts Gulf routes

[29] [37] [50] [55] [56] [59] AFPM ’26: US shipping, supply chains pressured as Middle East conflict raises costs | ICIS